How fast is too fast?

Is the pace of today's fundraising environment actually in the best interest of founders?

Welcome to issue #35 of next big thing.

We closed on Footwork Fund I in April, and it's been a very busy three months since. We've made our first three investments, in each case leading a Seed or Series A round of financing, and joining the boards of those companies. Via is the one that's announced thus far, and we can't wait to tell you about the other two.

As we've immersed ourselves in these investment decisions, each of which unfolded over the course of a few weeks, I've been reflecting on the current fundraising landscape. If I could summarize the environment in one word it would be "fast."

In my eleven years in venture capital, I've never experienced a market that's moving as quickly as it is at present. And in conversations with fellow investors, it seems we all feel the same way. Founders are going out to raise a new round, and within weeks, if not days, have multiple term sheets. So what's driving this speed? There are of course benefits to founders and investors for rounds to move faster. But what are the costs? How fast is too fast? Here are some of my thoughts.

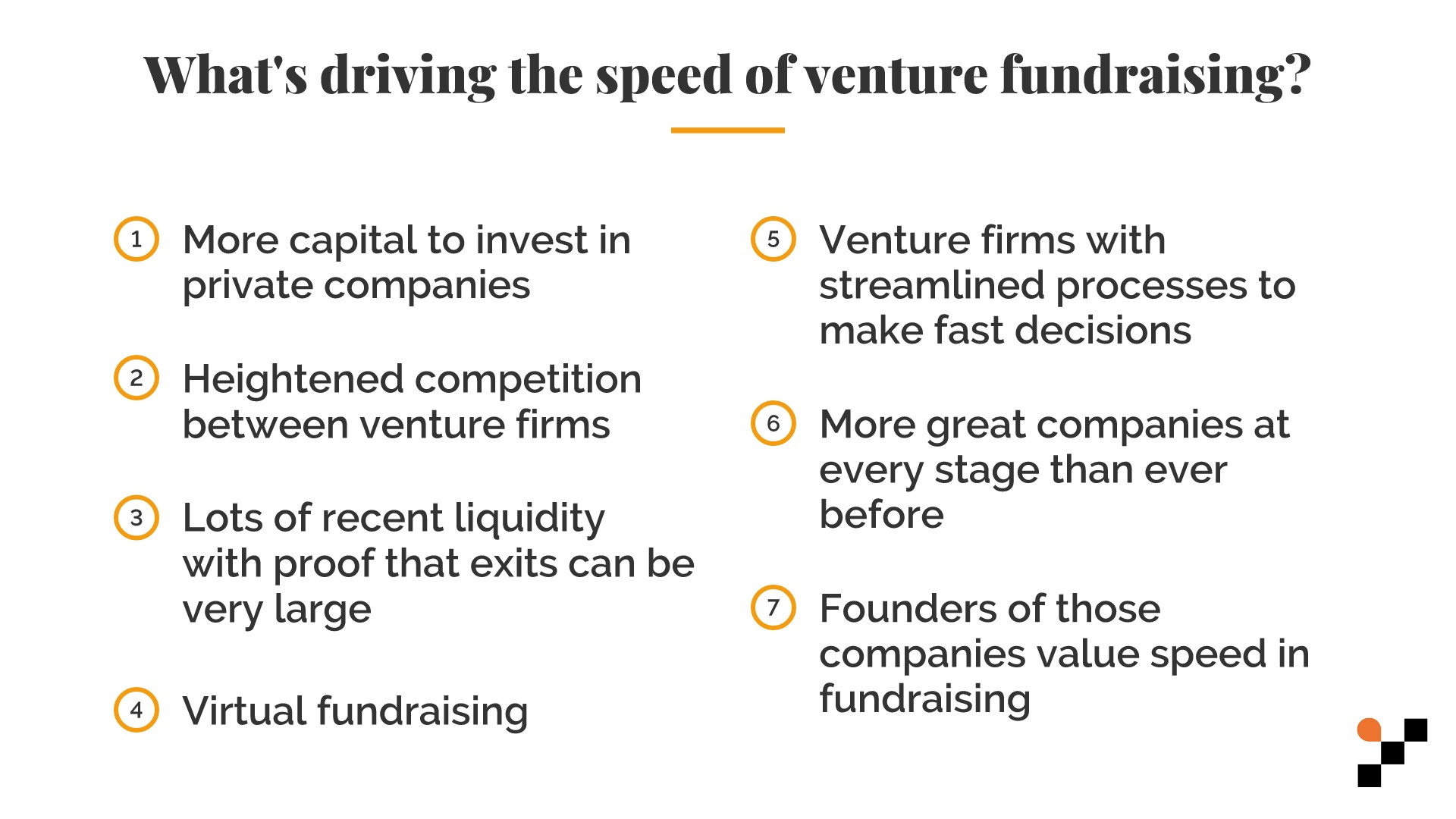

The Speed of Venture Fundraising

Venture capital rounds are being raised faster than most of us have ever experienced, across every stage. Here are seven factors that have led to the increase in speed:

1. More capital to invest in private companies.

Capital is being deployed by venture firms at a record rate. PitchBook-National Venture Capital Association (NVCA) data from Q2 2021 shows as much, with $150B invested by venture firms in the first half of 2021.

$150B is more than was invested in any calendar year except for 2020, so 2021 looks like it will be far-and-away the largest ever year of venture capital investment in private companies in the U.S.

Venture firms themselves need to fundraise from limited partners (LPs), and 2021 will be a record year on this dimension as well, with over $100B committed by LPs to venture funds.

2. Heightened competition between venture firms.

There’s more venture capital than ever to invest in private companies, and that is leading to heightened competition between firms to invest in them. Speed is one key vector on which a firm can compete to win the deal, along with valuation, value add, relationship, and other dimensions of founder-investor fit. There are plenty of examples of funding rounds this year that have unfolded in days as a result of heavy competition — Poparazzi’s Series A, for example, was reported by Eric Newcomer and Alex Konrad at Forbes to have taken place in a few days after launch, with Benchmark and Andreessen Horowitz fighting to win it.

3. Lots of recent liquidity with proof that exits can be very large.

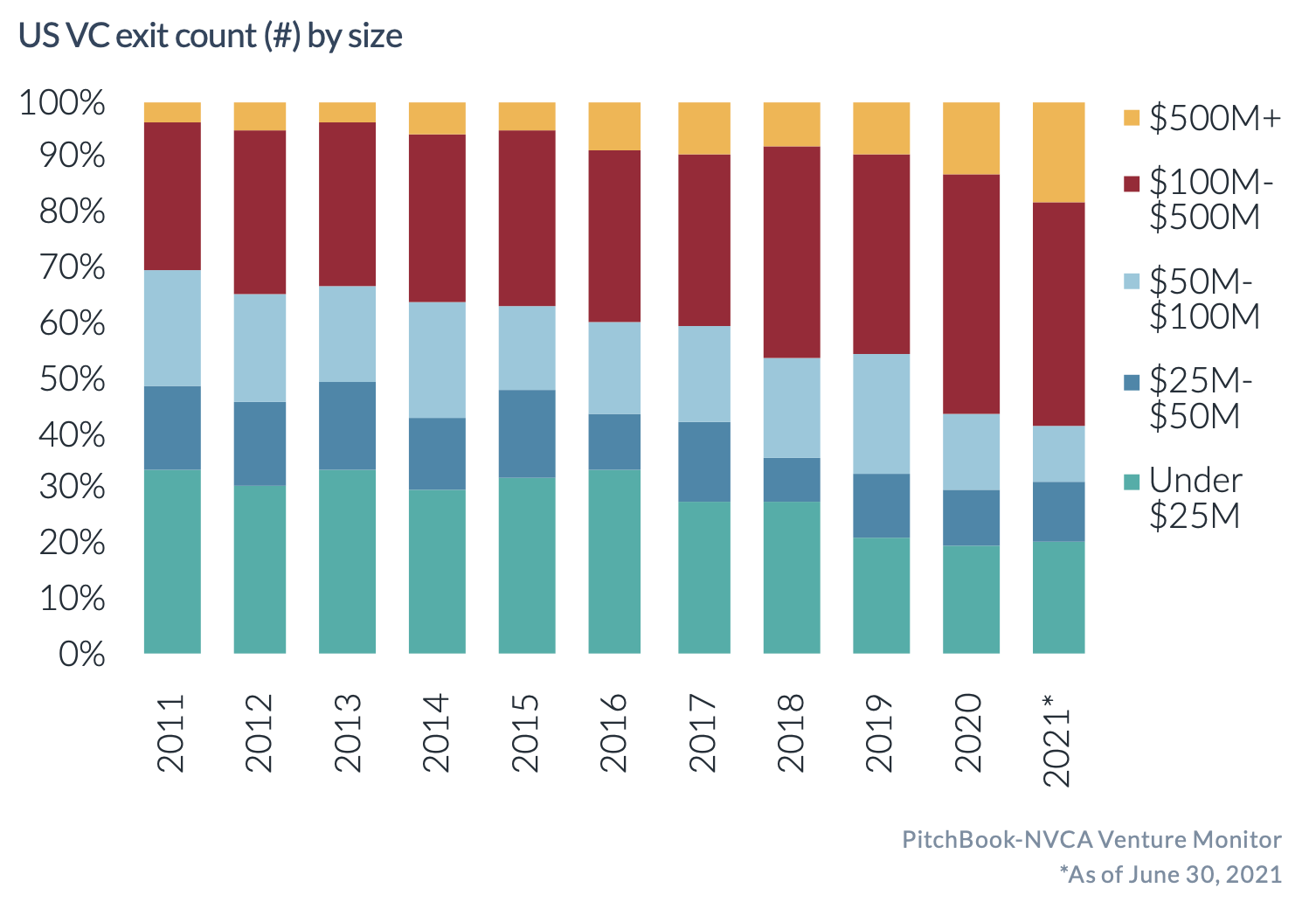

A key factor driving the record speed of venture financings is that investors are buoyed by the amount of recent liquidity via IPOs and M&As. 2021 is once again a record year in this respect, with more than $300B in exit value in the first year of the year, more than in any other full calendar year of the past decade.

The exits have also become larger in size, with many more companies exiting at above a $500M valuation in 2021 as a percentage of total exits.

All of this makes investors more willing to invest in new companies, and to justify moving at a rapid pace to make the investment. It’s also leading to the justification of higher valuations. Frank Rotman at QED Investors had a great Twitter thread last week unpacking this aspect of today’s fundraising environment, and much of what he shares applies to this discussion:

4. Virtual fundraising.

The shift to entirely virtual fundraising due to the pandemic has led to the ability for investments to happen faster. Removing the friction of travel and in-person meetings has sped up diligence on the part of investors and fundraising timelines as a result. Though founders and investors are meeting in-person again, if even one firm is able to make a decision entirely virtually, without meeting in-person, it forces others to adjust and operate on a similar timeline.

5. Venture firms with streamlined processes to make fast decisions.

From Tiger Global to solo capitalists, certain venture investors’ decision-making processes are very fast, and that has forced much of the industry to increase its pace. Larger firms point to the ability for general partners to make “single trigger” decisions, without needing to have the rest of the partnership on board, as a way to make faster decisions and win over founders. Smaller firms can usually be more nimble with fewer decision-makers around the table. These adjustments from investors are fueling the fast paced fundraising environment. Semil Shah at Haystack summarizes (or overhead someone else summarize) the sentiment on many investors’ minds well:

6. More great companies at every stage than ever before.

It’s worth noting that the companies being funded are oftentimes warranting quick fundraises because of their quality. What I see in today’s early-stage market is more companies with impressive fundamentals such as revenue growth, retention, strong unit economics, and quality teams than I’ve ever seen before. My friends focused at the later-stage say the same thing — that while companies are getting funded quickly and at higher valuations, the quality of businesses they’re seeing has gone up too, and of course, as stated above, the data on the size of exits going up backs up this anecdotal data as well.

7. Founders of those companies value speed in fundraising.

Finally, none of this would matter if founders didn’t value speedy fundraising. Less time fundraising means more time building the company. Having a quick fundraise can lead to more competition between investors (whether real or perceived). More competition can lead to a higher valuation and better terms. Speed can be an indicator of an investor’s conviction. Higher conviction investors can be value additive to the company in the good and bad times. All of these are benefits of fast fundraises.

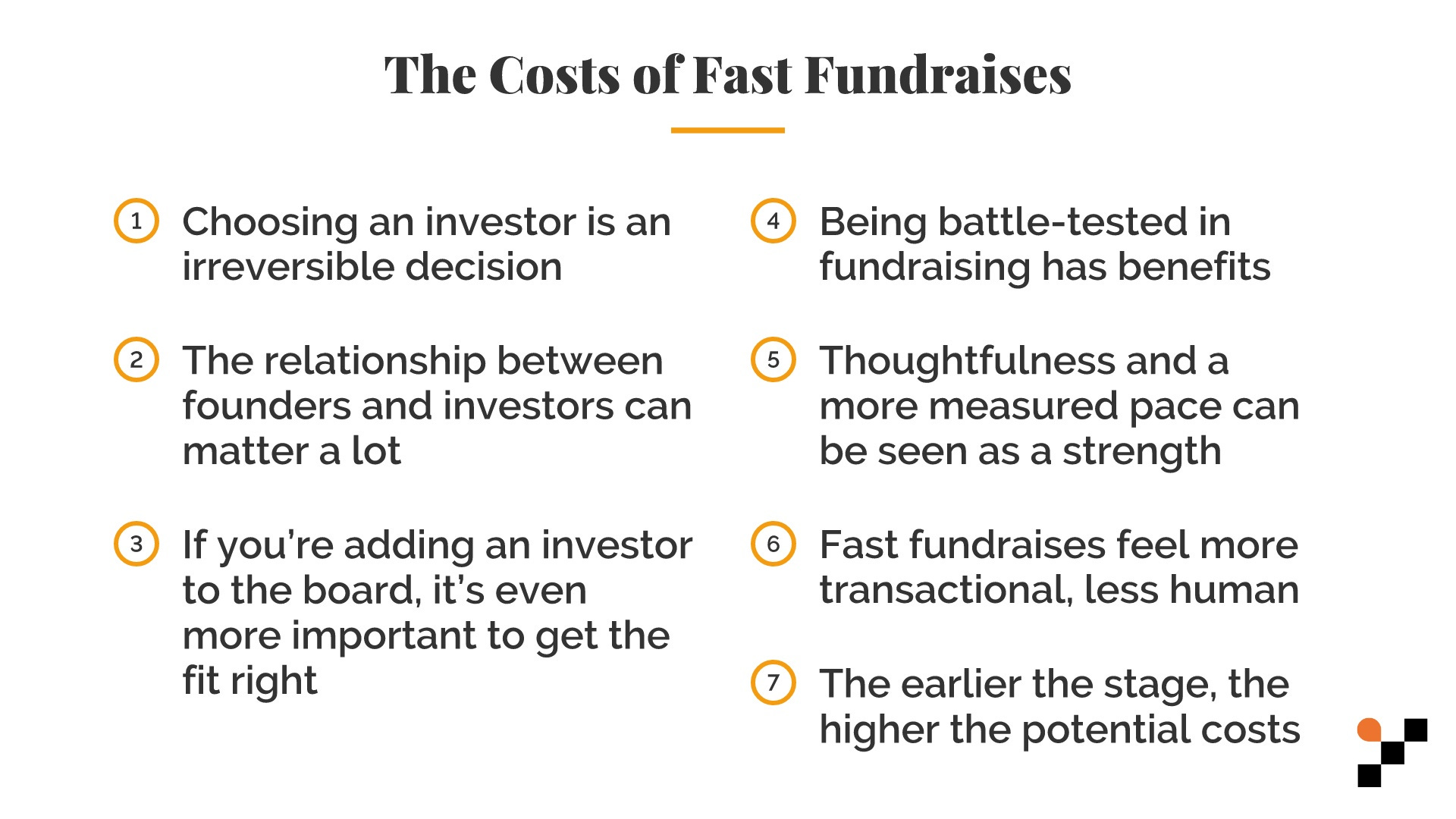

The Costs of Fast Fundraises

While there are lots of benefits of fast fundraising for founders, as well as a few for investors — for example, investors spend less time twiddling their thumbs in this market; they can invest or move on to the next opportunity in days or a few weeks, versus spending a month on diligence only to pass — there are several downsides that I believe not enough founders and even some investors consider.

1. Choosing an investor is an irreversible decision.

Firstly, it’s very difficult for companies to get rid of their investors, so for all intents and purposes, a fundraising decision is an irreversible decision.

2. The relationship between founders and investors can matter. A lot.

Why does the irreversibility matter? Because the relationship between founders and investors can matter a lot. If you’re making a decision in days, do you know if you really have founder-investor fit? Are you aligned on the same principles and values? Do you communicate well with each other? How does this investor behave when times are tough? The challenge with compressed fundraising timelines is that it’s hard to have a good sense for these answers going into what can become a very long relationship (the median time-to-exit is over 8 years!). Fred Wilson at USV summed this up well in a recent post, The Bad Marriage Problem:

We know that bad marriages are hurtful to everyone, not just the spouses. Companies that have dysfunctional founder/investor relationships suffer from them. And the shotgun marriage environment we are operating in right now (and for the foreseeable future) will likely create more of them.

3. If you’re adding an investor to the board, it’s even more important to get the fit right.

A typical private company board member has several governance rights — information and regular reporting from the company, a say in compensation for all employees, approving any future fundraises, a vote in additions to and subtractions from the board, and hiring and firing the CEO. The relationship with any investor is important, but the relationship with an investor you’re adding to the board, both with that individual and with the firm, is crucial to get right. Your board is your proverbial dining table — who do you want seated there for many years to come? Getting this right can increase your company’s value, and getting it wrong can be value destructive. A cost of today’s fundraising environment can be the inability to suss this out, by doing references and just spending time together, to make an informed decision.

4. Being battle-tested in fundraising has benefits.

While slow fundraises can be painful and distracting from the more important tasks in building the business, they can also push founders and operators to be better and more driven to succeed. Feedback from fundraising can be a gift; perhaps there is a key question that needs to be answered by the next round, or a risk that can be mitigated to improve the likelihood of success. Perhaps there’s even some correlation between tough fundraises and ultimate success — check out this thread by Sundeep Peechu at Felicis, which includes an interesting tidbit on investor governance and structure, relevant to the prior point:

5. Thoughtfulness and a more measured pace can be seen as a strength.

I’ve found myself wondering during fast-paced fundraising processes: “why are these founders so determined to close the round quickly?” Sometimes it’s just because they know they have a great business, have a lot of demand to invest, and want to move on. But the desire to move incredibly quickly can sometimes be borne out of insecurity. On the other hand, when founders are thoughtful about who they want to partner with, and are willing to move at a less-than-breakneck pace to figure out the right fit, I often see this as a sign of strength. It increases my excitement about these founders, because they can strike me as better business builders.

6. Fast fundraises feel more transactional, less human.

I very much want relationships with founders that are human, not transactional. Fast fundraises can often feel the opposite, and set the tone for the relationship to follow. It’s worth thinking about your cultural values and principles, and whether your fundraising process matches them.

7. The earlier the stage, the higher the potential costs.

When a company is in its infancy, there’s more to build and de-risk. To me, this makes the decision of who you bring on as your earlier stage investors more important than at the later stages, when your business is more established, and when you hopefully already have investors around the table with whom you have a strong, trusted relationship.

This isn’t meant to be an out-and-out critique of the fast fundraising environment. Fundraising is mostly a means to an end; ultimately the success and failure of a company will be much more about the execution on product, sales, marketing, hiring, and every other dimension of the company, not just fundraising. And, as mentioned, there are lots of benefits of today’s fast and efficient market. But I hope this helps founders, investors, and others in the ecosystem think twice about optimizing entirely for speed in the fundraising process. Sometimes fast can just be too fast.

I started next big thing to share unfiltered thoughts. I’d love your feedback, questions, and comments!

👇🏽 please hit the ♥️ button below if you enjoyed this post.

It mostly works for the founders with the right geography, colleges, and/or employment experience in fancy unicorns. The other 99.99% of the founders can't feel this gold rush. At all :)

The biggest reason is poor deal sourcing techniques ( hardly any science and only network) leading to the same network, same deals and an artificial access based competition. VC deal sourcing is the most unscientific procurement. The gloating over warm introductions makes the VC central and not the deal, idea or founder and therefore not the asset class. As a founder, I find the underlying assumptions difficult to comprehend logically.